Insurers know their customers’ lives are being shaped and transformed by new technologies. These technologies are also rapidly transforming the insurance industry, which is undergoing an ecosystem disruption, largely caused by technology-driven competitors and new entrants. As the market changes, insurers are facing growing pressure to adapt and reinvent themselves.

Shift from viewing emerging InsurTechs as opportunities rather than threats

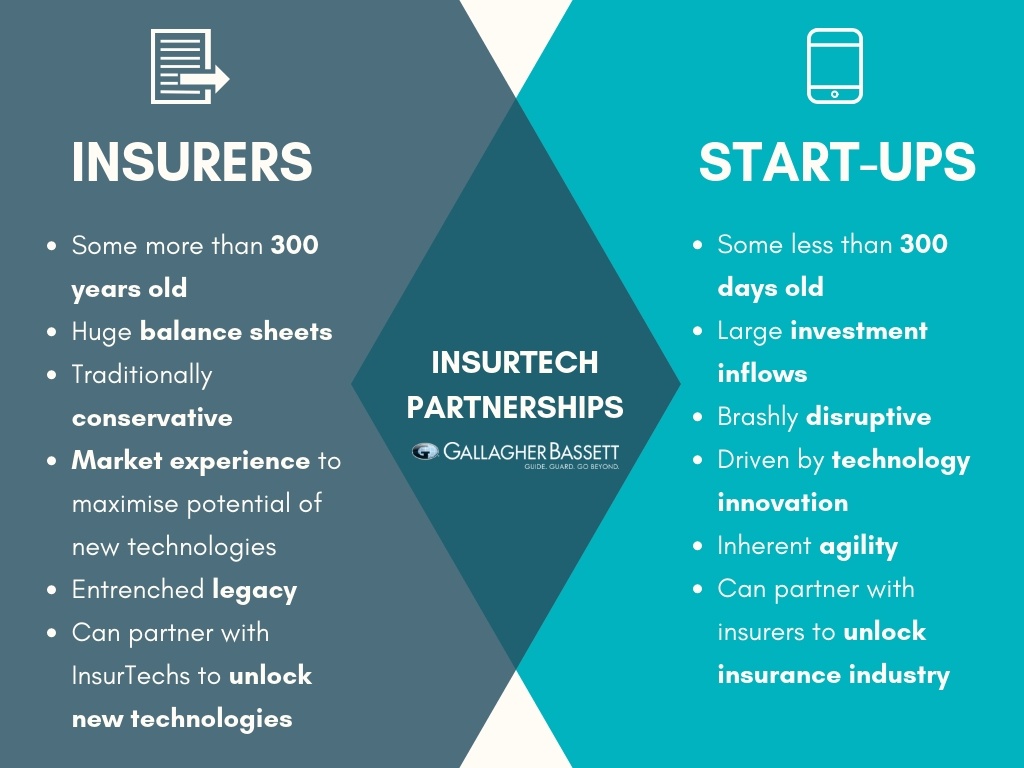

The emerging Insurtech (or “Insurance Technology”) industry, is gaining strong traction, with many start-ups developing new business models and enhancing customer experiences. PWC’s InsurTech report highlighted that 56% of insurance companies surveyed felt that between 1% to 20% of their revenues were risk to InsurTechs.

Insurers are becoming increasingly aware of the opportunities of partnering with emerging InsurTechs. Through strategic partnerships, traditional insurers attain economic benefits and overcome challenges that they have traditionally faced.

InsurTechs offer alternative ways of addressing customer needs, because of their data-driven experience models, agile structures, risk-taking mindsets and streamlined operational costs. They also have inherent advantages to launch new business models that traditional insurance companies are unable to do internally.

Despite being digitally native and being able to face insurance problems without past assumptions, InsurTechs typically have limited knowledge of regulatory environment, financial strength and claims data to accurately price and underwrite risks.

Traditional insurers are highly experienced with concrete institutional knowledge of the industry. They are well aware of the common pitfalls and challenges of operating in the industry, and have extensive experience navigating complicated regulations that govern the sector. Insurers can therefore use their extensive industry knowledge to assist InsurTechs to optimise their technology.

Strategic partnerships allows traditional insurers to focus on what they do best, insurance. Through the use of new technologies, InsurTechs can make insurers more efficient through use of new technologies and empower them to drive digital disruption.

Strategic partnership is the key for both traditional insurers and InsurTechs to achieve success.

How do customers benefits from partnerships between insurers and InsurTechs?

Customers are becoming increasingly tech savvy and their expectations for insurers reflects this. With their digital expertise, InsurTechs can help insurers leverage cutting-edge and emerging technologies to interact and reach customers where they are—mobile, online and 24/7.

InsurTechs have dramatically changed the traditional low-interaction model between the insurer and the customer.

With their expertise in emerging technologies, such as artificial intelligence (AI), the Internet of Things (IoT), blockchain, big data and analytics, InsurTechs can offer solutions for the challenges insurers are facing in this increasingly competitive and digitised space. A strategic partnership allows insurers to leverage new technologies to enhance customer engagement and adapt their product offerings.

InsurTechs and traditional insurers, can combine their knowledge and expertise to improve personalisation of their services. This can be achieved utilising their understanding of customer needs and taking advantage of real-time data from connected devices, such as wearables.

Through deepening relationships with their customers, a strategic partnership furthermore offer insights into risks and enables traditional insurers to base premiums on highly specific risk assessments. It also enables proactive risk mitigation services and the ability to provide timely care interventions.

A great example is Hiotlabs, a Stockholm-based InsurTech that offers ‘prevention as a service’ by using Internet of Things sensors to measure temperature and humidity inside buildings, allowing early detection of water damage.

Creating new customer touchpoints and revenue streams

By utilising a collaborative model with traditional insurers using Application Programming Interfaces (APIs), new customer touchpoints are created. By offering a variety of insurance apps, Application Programming Interfaces can assist insurers to deliver seamless customer protection and subsequently access new revenue streams.

An example of successful integration of Application Programming Interfaces was achieved by Matric. They use API to integrate with third-party mortgage platforms and home insurers’ systems. When clicking the ‘request quote’ button, already 95% of the details required to offer a home loan quote are sent out automatically to the carrier. This means that the customer only has to answer a small number of additional questions for a near-instant quote.

Assisting insurers to streamline processes

Partnering with InsurTechs can allow traditional insurers to streamline their processes and achieve operational efficiency through use of technology, for example, by implementing cognitive document processing. InsurTechs are beginning to offer ways to utilise Artificial Intelligence and Robotic Process Automation to automate elements of insurance value chain processes.

For example, Expediente Azul, a Mexico-based InsurTech, offers a mobile and web tool that assists insurers to capture, analyse and store insurance claim documents in the cloud, therefore managing end-to-end insurer and customer interactions during claims processing.

Blockchain technology is another key disrupter as it allows secure, seamless and transparent data sharing and storing. This can facilitate more effective fraud prevention and detection. In addition, Blockchain-based smart contracts can lead to instant processing of claims and subsequently quicker payouts. This allows traditional insurers to streamline claims management.

Facilitating an effective partnership

The growing interest in InsurTech partnerships is reflected by Accenture research, which found out that 44% of insurers globally intend to pursue digital initiatives with insurance industry start-ups over the next two years. They also discovered that 31% intend to work alongside start-ups from outside their industry.

The insurance industry must be proactive and demonstrate a willingness to engage with InsurTechs to create a mutually beneficial and sustainable model.

For InsurTechs, accessing traditional insurers’ extensive customer bases, industry knowledge and market experience is the key to scaling their offerings.

Through effective collaboration, strategic partnerships can allow traditional insurers to attain better customer satisfaction and retention, new revenue streams and a streamline process that allows for operational efficiency.

Nevertheless, it’s vital for the Insurer to find the most appropriate strategic InsurTech partner. This may be particularly challenging as technology is not their area of expertise.

The key is to therefore find a partner with a capacity to understand their customer journey and have the ability to work together long-term.